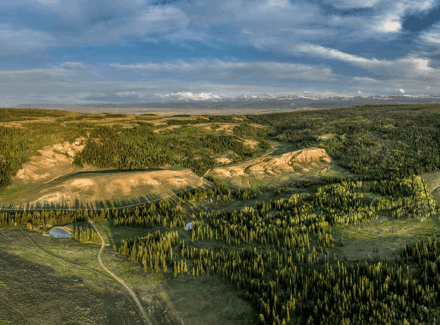

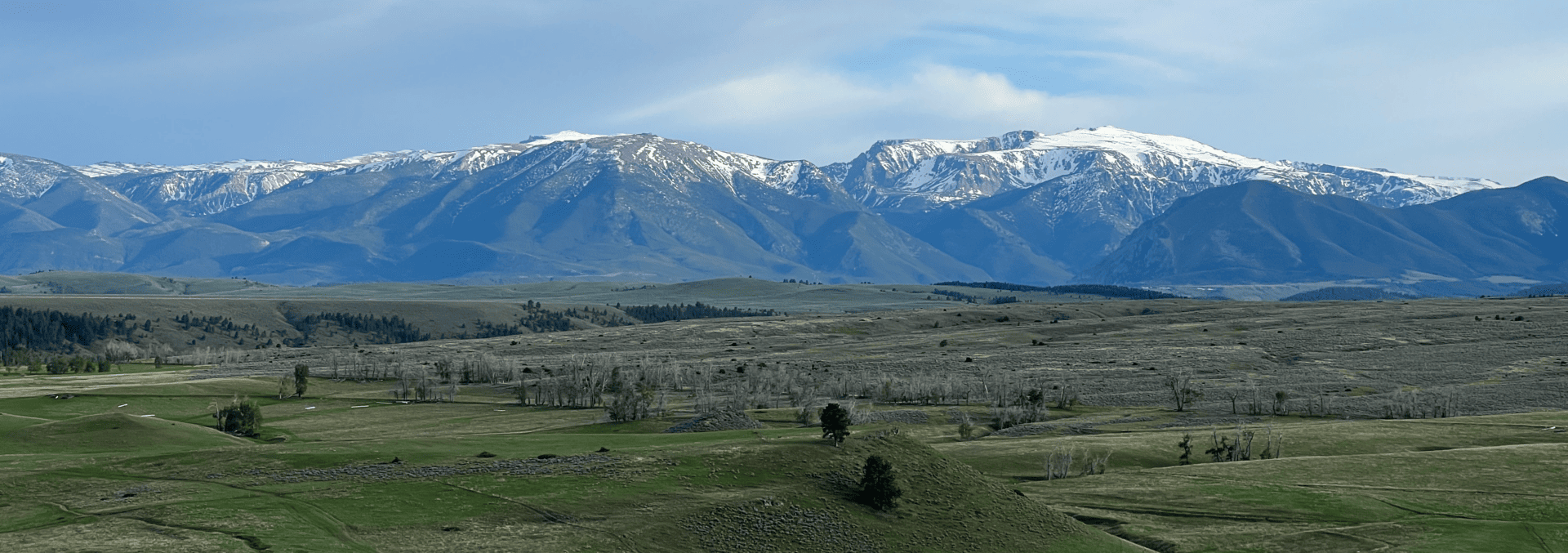

Rogers Wash Gold Mine

Wickenburg, Arizona

Positioned near Wickenburg, Arizona, in a region renowned for its mining legacy, this fully permitted placer mine project offers rare investment-grade potential backed by confirmed in-ground values exceeding $118 billion. A BLM-approved Mining Plan, completed Environmental Assessment, and secured water rights ensure the project is fully de-risked and ready to advance. With multi-phase development underway and significant expansion upside identified, this is a generational resource opportunity.

Lakes of Gibbons Creek

College Station, Texas

This Texas ranch is a world-class and extraordinary example of natural resource and rangeland restoration undertakings over the course of several decades following an intense use of portions of the surface to secure lignite. The resources that were put to work on this restoration project have resulted in an extensive ranch with rolling rangelands of both improved and native grasses, heavily wooded bottomlands (and some hilltops), and incredible water features.

Crestonio Ranch

Hebbronville, Texas

The Crestonio Ranch, a premier 11,965± acre South Texas property, features exceptional quail hunting and a high-fenced 9,600± acre area with a top-tier deer herd, including multiple 200+ inch bucks. It offers superb dove and turkey hunting, efficient cattle operations, and luxurious amenities for entertaining. This meticulously crafted ranch combines luxury with functionality, making it a premier Texas playground and working ranch.

Zortman Landusky Gold Resource Property

Zortman, Montana

Through the work of Ruby Gulch Mining Company, the Gold Reserve Mining Company, and Pegasus Gold, this property was consolidated from mineral owners. Geologists estimate that only 20% of the gold and silver has been harvested from this Montana land, leaving plenty of reserves for investors or operators. The property is characterized by planted reclaimed pit mining sites, cliff bands, timbered ridges, and clearcuts, creating a bighorn sheep sanctuary and a mule deer and elk habitat.

Silver Springs Cattle Ranch

Tenino, Washington

Located in Thurston County, Washington, this property combines high-value conservation potential, mineral resources, and income generation. Its diverse habitats support federally protected species and are eligible for mitigation credit development. The land also holds vast sand and gravel reserves with permits underway, plus rail access for distribution. Current leases—ranging from composting to solar—provide steady revenue and long-term flexibility.

Cross Keys Ranch

Madras, Oregon

Established in 1879, Cross Keys Ranch spans 66,000± acres, blending history with a premier cattle operation. Rated for 1,200–1,500 cows, it features irrigated hay ground, vast grazing land, and stunning landscapes from the Cascade Mountains to the Deschutes River. Offering hunting, fishing, ATV trails, and more, it includes a luxury owner’s home, guest cabins, a rodeo arena, and historic buildings. With unmatched beauty and versatility, this ranch is a rare and historic opportunity.

Dome Mountain Ranch

Emigrant, Montana

This stunning ranch has incredible views in all directions ranging from mountain ranges, the Yellowstone River, the famed Paradise Valley and into Yellowstone National Park. The land transitions through three ecosystems from the river bottom riparian area to the Absaroka Mountain Range’s forested mountains. There are also three lakes on the ranch. The ranch is well improved with a beautiful log home and guest homes and the Dome Mountain Guest Ranch structures along the river.

Leadore Angus Ranch

Leadore, Idaho

Set in eastern Idaho, this extraordinary river-to-mountain operation stretches from the fertile banks of the Lemhi River to the rugged peaks of the Continental Divide. The fully integrated cattle program supports 2,000+ cow/calf pairs year-round, with 2,900± irrigated acres producing thousands of tons of hay annually. Over eight miles of private Lemhi River frontage offers exceptional trout fishing, while expansive habitat supports trophy elk, deer, antelope, moose, and bighorn sheep.

Kincaid Ranch

Uvalde, Texas

This South Texas property along the Frio River offers agricultural production, hunting, and recreation. Rolling brush country, fertile soils, and irrigated farmland support cattle and wildlife, including deer, quail, and turkey. A river house with an outdoor gathering space overlooks scenic pools, perfect for family gatherings. Conveniently located, this rare offering is offered in its entirety or as smaller east or west portions, blending history, utility, and natural beauty.

Cheyenne River Ranch

Rapid City, South Dakota

Cheyenne River Ranch spans 15,920± total acres just 30 minutes from Rapid City, South Dakota. It supports significant cattle and buffalo operations with 14,842± deeded acres, grazing permits, and rich water resources from Rapid Creek. Improvements include homes, working facilities, and 30 miles of pipeline. Fertile hay ground and trophy wildlife add to its value. This rare offering combines scale, productivity, and recreation—priced below multiple appraisals.

Silver Ruby Ranch

Sheridan, Montana

A premier river-to-mountain property in Montana’s Ruby River Valley, offering exceptional privacy, water, and wildlife. Both sides of a blue-ribbon trout river, a private spring creek, and a scenic pond system create outstanding fishing and waterfowl habitat. The land balances productive agriculture and conservation, with abundant elk and deer and nearby public land access. Improvements include a striking main residence, guest home, and manager’s home, all set in a beautiful, secluded landscape.

The Bird Estate

Rogue River, Oregon

Architecturally significant and featured in Architectural Digest, this neoclassical estate offers a level of design and craftsmanship rarely found in the luxury market. Set amid manicured grounds and wooded privacy, it includes formal entertaining spaces, an amphitheater with water features, terraced outdoor living areas, an Olympic-sized pool, guest accommodations, a vineyard, and equestrian facilities. It is well-suited for private use, hosting, or income-producing events.

Criterion Ranch

Madras, Oregon

This extraordinary offering combines nearly 50,000± acres of prime Central Oregon cattle and hunting land. With irrigated meadows, reliable water, and excellent grazing, it supports strong hay and cattle production. Trophy elk, mule deer, antelope, and upland birds enhance its sporting value, along with fishing and extensive recreation. The property includes high-end residences, operational facilities, and event venues, offering turnkey income from ranching, outfitting, and hosting.

Ironside Castle Rock Ranch

Juntura, Oregon

Spanning three Oregon counties, this working cattle ranch rises over 4,200 vertical feet through irrigated meadows, sagebrush uplands, rugged river canyons, and timbered high country crowned by a privately owned summit. Nearly 25 miles of private river and stream corridors hold fisheries so remote that trophy trout go largely undisturbed, while a private riverside hot spring lends rare distinction. Three homes and working facilities anchor a ranch built for legacy ownership in the American West.

Foley Butte Ranch

Prineville, Oregon

Extreme privacy without sacrificing a convenient location in Oregon! This ranch offers premier big game hunting and excellent summer grazing in the Ochoco Mountains, all within driving distance to everything Central Oregon has to offer. With over 140 miles of creeks and streams, beautiful meadows, outstanding timberland, and 8 landowner preference tags for Rocky Mountain bull elk and buck mule deer.

Crazy Elk Ranch

Belgrade, Montana

This property features a stunning 9,690± SF dream home designed by Locati Architects with views of Bozeman’s Gallatin Valley, the Bridger Mountains, and the Missouri River Valley. This escape in Montana includes a guest home, a barn for toys and gear, a rustic hunting cabin, and a ranch manager’s home. The striking improvements are only bested by the thousands of deeded acres to recreate on, already divided into 21 parcels.

Sage Creek Ranch

Fort Bridger, Wyoming

This premier big game hunting retreat is surrounded by public lands, offering rare seclusion and recreation. With year-round streams, a private reservoir, and direct access to national forest, it supports abundant wildlife, varied terrain, and boundless outdoor adventure. Rich in natural resources and scenic beauty—from open rangeland to aspen-covered high country—it perfectly captures the spirit of the Western lifestyle.

McWilliams Gold Claim

Talkeetna, Alaska

This Alaska Gold Claim offers the opportunity to own a piece of Alaska Gold Rush history with investment potential from the patented mineral rights. The ownership includes 41 gold claims along the Chunilna and John’s Rivers. Located 34± miles N/NE of Talkeetna, the property offers breathtaking views of Talkeetna and Denali Mountain ranges. With more annual snowfall than in Vail, CO, winter activities are countless, and summertime outdoor activities provide the authentic Alaskan experience.

Jefferson River

Legacy Ranch

Three Forks, Montana

A six-generation, family-owned property with roots dating to 1855, this ranch reflects a deep connection to Montana’s history, including ties to Lewis and Clark’s 1805 expedition. Along the Jefferson River, it offers strong agricultural capability, conservation potential, abundant wildlife, and excellent hunting and fishing. Scenic mountain views, convenient access, and proximity to Three Forks and Bozeman deliver functionality and a true Montana ranch experience.

Ashley Lake Mountain Estate

Kila, Montana

This Montana estate combines natural beauty and refined living. It has over 1,100 feet of Ashley Lake frontage, 7.5± miles of private trails, and custom improvements crafted with timeless design. The property offers year-round recreation, from hiking and horseback riding to skiing and snowshoeing, all amid forested ridges and mountain views. Located minutes from Kalispell, Whitefish, and Glacier National Park, it provides seclusion, convenience, and unmatched opportunities.

Wylie Mountains Ranch

Van Horn, Texas

This ranch covers nearly the entire Wylie Mountain range in West Texas, offering diverse habitats like desert grasslands, brushlands, foothills, and expansive canyons. The ranch supports wildlife such as mule deer, pronghorn, and quail, alongside exotic species like elk and aoudad. Improvements include a 3/2 owner’s home and manager’s residence. Water is sourced from 6 wells and runoff tanks. The ranch includes acres of mineral rights and leased acres from the Texas Pacific Land Trust.

Slash Broken Box Ranch

Steamboat Springs, Colorado

A diverse Colorado ranch, ranging in elevation from 6,700′ to 7,600′, includes over a mile of the legendary Elk River on the southeast boundary, rolling grazing land in the middle acreage, and the northwest boundary sits at the base of Sleeping Giant Mountain. Big game hunting for elk, mule deer, and pronghorn is present during the fall season. Due to the senior Elk River water right, the ranch produces in excess of 300 tons annually and can graze 200 AUMs. Multiple springs serve small ponds.

Uncle Bill’s Farm & Ranch

Las Nutrias, New Mexico

Nowhere in the Southwestern US will one find a more productive combination of farm & ranch at this kind of price, and with New Mexico’s low property taxes! An incredible amount of water is attached to this farm. An abundance of grazing with large-herd-carrying capacity makes up the range lands, with the price-per-animal-unit being lower thanks to State and BLM leased lands. Both properties are wildlife strongholds with biodiversity that lends itself to activities ranging from trophy big game hunting to some of the finest birdwatching in NM.

Red Barn Ranch on Lake Bob Sandlin

Winnsboro, Texas

Rolling piney woods, sweeping water views, and rare Lake Bob Sandlin frontage set the stage for an exceptional East Texas retreat. Multiple turnkey homes, enhanced wildlife habitat, productive wetlands, and abundant surface and groundwater create immediate enjoyment with long-term potential. Just under two hours from Dallas, this property blends solitude, recreation, and legacy appeal in a truly timeless setting.

Sweetwater Ranch

Gypsum, Colorado

This Colorado ranch contains irrigated hay meadows across the entire ranch from low to high elevations & a perfect mosaic interspersed habitat including cottonwood, willow, aspen, gambrel oak, and evergreen forests. The abundant forage, plentiful water resources, and diverse habitat provide a natural preserve for the area elk herd and mule deer populations. The ranch includes over 1.5 miles of fishable Sweetwater Creek, multiple stocked reservoirs, and a diverse portfolio of senior water rights.

Rocking Chair Ranch

Philipsburg, Montana

This expansive holding supports a productive cattle operation across a diverse and functional landscape. Riparian meadows and irrigated fields transition into rolling rangelands and conifer forest, creating a balanced mix of forage, cover, and seasonal flexibility. More than two and a half miles of Flint Creek run through the property, sustaining a healthy brown trout fishery and strong riparian habitat. Elk, deer, and other wildlife regularly use the uplands and creek corridor.

K Bar J Ranch

La Pine, Oregon

This Oregon property offers seclusion and wildlife habitat while bordering La Pine. Highlights include a log home with mountain views, a pond with a dock, and the Little Deschutes River. The main site features a detached carport, office, horse barn, hobby barn, additional homes, and historic barns. The ranch spans 2.7± miles along the river and includes pine forests and meadows with diverse wildlife. It offers various land use options and the perfect retreat for privacy and recreation.

Bighorn River Ranch

Custer, Montana

An hour from Billings, Montana, this property boasts 7.5+ miles of Bighorn River frontage. Endless fishing opportunities include walleye, sauger, smallmouth bass, catfish, ling, and rainbow and brown trout. For the hunter, pursue bull elk, white-tailed and mule deer, antelope, pheasants, turkeys, Hungarian partridge, and sharp-tailed grouse. This ranch is renowned for its waterfowl hunting. Boasting 5 center pivots/wheel lines and flood irrigation, the soils are high-producing.

Burnt Hollow Ranch

Deer Lodge, Montana

About 10 minutes to Deer Lodge, Montana, this recreational paradise sits up against the Boulder Mountains. Creeks and springs flow through as animals traipse by on their way to contiguous National Forest, bordering the property for almost nine miles. The property features an 8,774± SF, 3 bed, 5 bath home, a second home, additional residences, hunting cabins, and outbuildings. Agricultural operations include irrigated hay ground, pivots, wheel-line and flood-irrigated fields, and fenced pastures. State and Forest Service grazing leases total 4,100± acres.

Sendero Verde

Edwards, Colorado

Unbelievable Colorado mountain retreat with includes two air-conditioned homes. With views of the Gore and Sawatch Mountain Ranges, the 14,419-square-foot home has a step-less entry, walls of windows capturing the magnificent views, two four-car garages, and a second 2,636-square-foot caretaker home with two bedrooms, three baths, and an office. Outside has a well-stocked fishing pond and 10 miles of custom-built trails for hiking, snowshoeing, or snowmobiling.

The Schmidt Ranch

Bozeman, Montana

This property offers an unparalleled recreational retreat just 10± minutes from downtown Bozeman, Montana, capturing the essence of Montana’s rugged beauty with rolling aspen hills, evergreen forests, meadows, and creeks, all with breathtaking views of the Bridger Mountain ridgeline to the north, along with sweeping 360-degree mountain views that complete this scenic landscape. The property is a haven for wildlife enthusiasts, featuring abundant deer, elk, bear, moose, and diverse bird species.

Stillwater Legacy Ranch

Nye, Montana

Located in the scenic Stillwater Valley near Nye, Montana, this legacy property features 1.65± miles of the Stillwater River frontage, complemented by 0.7± miles of both sides of the West Fork Stillwater River flowing through the heart of the ranch. With irrigated and sub-irrigated pastures, thermal springs, modest homes, abundant wildlife, and panoramic mountain views, it offers exceptional recreational opportunity, agricultural utility, and natural beauty in a private and peaceful setting.

Lone Woman Mountain Ranch

Driftwood, Texas

This Hill Country ranch stands out for its strong water features, healthy wildlife habitat, and usable improvements. A stocked pond, a second pond, creeks, springs, and seasonal waterfalls support both recreation and native game. Two residences, wells, septic systems, electric meters, and an established road network add immediate function and flexibility. With no zoning, no ETJ restrictions, and adjacency to conservation land, it offers privacy, freedom, and long-term appeal.

Ennis Lake Ranch

Ennis, Montana

Fay Ranches is proud to announce the featured sale of The Ennis Lake Ranch, one of those highly coveted Madison Valley ranches. The Ennis Lake Ranch is both stunningly beautiful and located in a highly desirable area. As its namesake implies, Ennis Lake Ranch is one of the very few ranches with frontage on the lake, providing gorgeous views and boating fun.

West Boulder Ranch

McLeod, Montana

Nestled at the base of the Absaroka Mountains in south central Montana, the West Boulder Ranch is one of the most scenic and prolific sporting ranches in the Northern Rockies.

Continental Ranch

Freer, Texas

For the first time in 75 years, this Webb County, Texas ranch is available to new ownership. Known for its wild terrain, native whitetail deer, quail, and rich history, it offers prime fair-chase hunting with 80% low fencing and abundant wildlife. The land features rolling topography, two wet-weather creeks, and 14 water tanks, including stacked systems. With six cross-fenced pastures, working pens, and modest improvements, this is a rare chance to own a true South Texas sporting & cattle ranch.

Wild Goose Ranch

Steamboat Springs, Colorado

A rare South Valley estate offering privacy, luxury, and abundant water features, including a private waterfall, ponds, creeks, and brooks, all minutes from Steamboat Ski Area. Designed for multi-generational living, the ranch offers panoramic mountain views, cathedral ceilings, a gourmet kitchen, and spaces for entertaining. A private primary wing, guest suites, and seamless indoor-outdoor living highlight the residence, which integrates sustainable solar systems.

Elk Meadows Ranch

Big Sky, Montana

Elk Meadows Ranch is a stunningly beautiful, private recreational ranch, a great real estate investment and a gathering place for friends and family. A world-class ranch within minutes of a world-class ski resort, this unique quality makes it a rare one-of-a-kind asset.

Skistone Mountain Ranch

Steamboat Springs, Colorado

Commanding, unobstructed views of the Steamboat Ski Area set the tone for this exceptional Colorado mountain estate. The residence pairs massive hand-hewn log beams, soaring cathedral ceilings, sweeping staircases, and multiple fireplaces with generous spaces for gathering, guests, and recreation. Rolling meadows, aspen groves, dark timber, water features, trails, abundant wildlife, and substantial outbuildings create a private retreat just minutes from Steamboat Springs.

Mallard Rest

Webb, Mississippi

Mallard Rest has been the private Mississippi Delta duck hunting property of Memphis’s former cotton merchant William B. Dunavant, Jr for almost 40 years. This property has been featured in books, spoken of reverentially amongst duck hunting enthusiasts, and celebrated for decades as one of the south’s most productive and famous duck hunting properties. Mallard Rest is now available for purchase.

Berclair Ranch

Berclair, Texas

This Texas property, established in 1859 and managed by six generations, blends rich history with natural beauty. It features diverse landscapes, including rolling rangelands with live oaks and wildflowers and two creeks—Blanco and Mucorrera—offering scenic views and recreational opportunities. Home to abundant wildlife, the property also supports an active cattle operation. Improvements include working pens, hunting camps, and water sources, making it a versatile property for various uses.

Rocking Chair Ranch

Dubois, Wyoming

This legacy Wyoming property for sale offers multiple residential dwellings, a working ranch, and expansion options – all within a majestic setting. The property’s expansive and varied landscape provides year-round recreational activities such as horseback riding, ATV trails, big game hunting, making this ranch ideal for multi-generational or expansive families. The Rocking Chair Ranch also offers a fully operational cattle ranch, with a turn-key option available.

Branch Keyhole Ranch

Midvale, Idaho

Available for the first time in five decades, Idaho’s Branch Keyhole Ranch spans a vast expanse of undulating hills and fragmented waterways. With its eastern boundary adjacent to Payette National Forest, the ranch boasts 86,673± acres of grazing leases. The property includes around 600± irrigated acres (pivots & wheel line) and 600± acres of dryland farming. The ranch features three residences, corrals, and all the necessary infrastructure, epitomizing the classic Western cattle ranch setting.

La Arena Ranch

Raymondville, Texas

This South Texas property offers exceptional hunting and ranching opportunities just northwest of Raymondville and near Port Mansfield. Sharing fence line with the famed King Ranch, it features old-growth brush, fine sandy soils, and diverse wildlife, including whitetail deer, quail, dove, turkey, and abundant free-ranging nilgai. With quality fencing, pastures, ponds, five water wells, and an excellent road system, it combines strong recreational appeal with functional ranch infrastructure.

Plaza Blanca Ranch

Abiquiú, New Mexico

Set in the dramatic landscapes of Abiquiú, New Mexico, Shirley MacLaine’s property combines natural beauty with spiritual peace. Unique white sandstone cliffs made famous by Georgia O’Keeffe rise at the entrance, while vast pinyon/juniper forests & native grasses stretch across the land. A hacienda-style home with solar and wind power anchors the ranch, complemented by a caretaker’s home and barns. With national forest adjacency, abundant wildlife, and rich history, it offers a rare opportunity.

Purgatory Bend Ranch

San Marcos, Texas

This Texas conservation ranch offers diverse landscapes of live oaks, native grasses, bluffs, and canyons along Purgatory Creek. The property has been actively managed for wildlife, supporting whitetail deer, turkey, dove, and feral hogs. Water wells, troughs, and electrical services offer sustainable land stewardship and potential for future subdivision. Protected by two conservation easements, the ranch allows up to 6 building envelopes, making it an ideal long-term investment.

Moore Creek Gold Mine

McGrath, Alaska

Located on the Iditarod National Historic Trail in Alaska’s Yukon-Koyukuk Borough, Moore Creek Gold Mine spans 2,720± acres with 20 unpatented state claims. Renowned for placer and hard rock gold, the site has yielded gold nuggets up to 19 oz. Mining since 1911 has produced at least 53,990 oz of gold and 12,520 oz of silver. Rich in history and resources, it offers a rare investment opportunity in a remote, mineral-rich region, combining economic potential with Alaska’s rugged beauty.

Canyon Creek Ranch

Canyon Creek, Montana

Located near Helena, Montana, this exceptional cattle and recreational property combines modern functionality with authentic western character. Extensive updates to improvements and infrastructure enhance efficiency and support all aspects of ranch operations. Fertile pastures, trout ponds, and abundant wildlife create outstanding opportunities for outdoor recreation. With comfortable living quarters and panoramic mountain scenery, this property offers the ultimate Montana ranching lifestyle.

El Monte Gringo Ranch

McCook, Texas

Built from three historic South Texas ranch tracts in western Hidalgo County, this highly improved sporting property offers fertile soils, exceptional native habitat, abundant water, trophy whitetail management, strong quail and dove hunting, and a full suite of luxury improvements. With a major lodge, owner’s home, stocked ponds, wells, food plots, and turnkey operational infrastructure, it is suited for private enjoyment, corporate retreat use, or a proven commercial hunting operation.

Little Belt Elk Ranch

White Sulphur Springs, Montana

This historic and stunning Montana ranch is situated in the Little Belt Mountain Range and offers a nearly incomparable spectrum of wildlife habitats to attract game. The combination of grassy meadows, large basins, spring seeps, aspen groves, and mature timber provides shelter, food, and sanctuary for a plethora of species. Eagle and Sheep Creeks flow through portions of the property, which provide endless fishing adventures for the avid angler. It is set up for a large-scale Cattle ranch.

The Hideout Lodge & Guest Ranch

Shell, Wyoming

This acclaimed destination is internationally recognized for Western hospitality and equestrian experiences, earning accolades from major outlets and top ranch rankings. Known for advanced horsemanship and expansive riding terrain, it offers guests instruction and authentic immersion into Wyoming ranch culture. With luxury accommodations, extensive facilities, irrigated pastures, and a strong international reputation, it stands as a turnkey lifestyle investment and proven business enterprise.

Brass Lantern

Bozeman, Montana

Just over four miles from downtown Bozeman, this extraordinary Montana estate delivers the perfect balance of privacy and accessibility, with direct access to National Forest trails and the M Trailhead right at your doorstep. Reimagined in 2022, the 9,787± square foot residence offers seven bedrooms, vaulted great rooms, mountain views, and a showpiece kitchen built for serious entertaining. Outside, radiant-heated patios, a private pond, and a covered outdoor kitchen complete the picture.

Ekwortzel Legacy Ranch 1896

Nye, Montana

Originally homesteaded in 1896 and owned by the same family for over a century, this historic Montana ranch embodies the spirit of the American West. With pristine river frontage, natural springs, abundant wildlife, and productive meadows, it offers opportunities for ranching, recreation, and conservation. Free from zoning restrictions or conservation easements, it provides the rare freedom to build, preserve, or evolve the land while enjoying proximity to natural landmarks and Yellowstone.

Settle Ranch

Canyon Creek, Montana

This extraordinary ranch offers diverse landscapes, including forested mountains, sagebrush hillsides, aspen creek bottoms, irrigated hay fields, and natural grasslands. Located 25± minutes from Helena, Montana’s state capital, the property is a generational working ranch providing excellent wildlife resources, recreation, and natural beauty. Developed as a traditional Montana cattle ranch, the improvements comprise multiple residences, historic sheep barns, loafing sheds, and corrals.

Willowdale Ranch

Madras, Oregon

An extraordinary opportunity in the heart of the American West, this iconic ranch embodies the ideal blend of adventure, agricultural productivity, and natural beauty. Premier cattle and hay operations are supported by significant irrigation rights and supplemental wells. The ranch offers a private bass lake, outstanding big game hunting, abundant fishing, multiple homes and cabins, rodeo grounds, a trap and skeet range, and unmatched resources for a multigenerational Western lifestyle.

Corbly Mountain Ranch

Belgrade, Montana

The Corbly Mountain Ranch offers a wide variety of recreational pursuits from hunting, hiking, biking, horseback riding, and whatever your heart desires. With private and direct access to the forest service, the possibilities are endless. Only 25 minutes from downtown Bozeman and 15 minutes from the airport the location is convenient while being at the end of the road and very private. Along with great views and many building sites, the Ranch is a must-see.

T90 Cattle Ranch

Tenino, Washington

The opportunity to own a ranch of this size rarely comes up in Western Washington. The large open grassland area on the hill is the perfect place to build your dream home where you can enjoy watching the sunrise over the mountains. Enjoy a rural, secluded lifestyle with all the convenience of being close to amenities.

Carten Creek Ranch

Gold Creek, Montana

Montana’s beautiful Clark Fork River Valley is now a quiet ranching community and home to a unique Montana ranch. With its diverse and abundant wildlife population and rolling landscape, the property is a rare Montana property in a desirable location. A beautiful 3,000± square-foot off-grid log home rests on an open ridge, maximizing views of the valley below. From well-constructed mountain roads and trails and improvements, the ranch is the ultimate turn-key opportunity.

Northern Plains Ranch

Belle Fourche, South Dakota

This is an opportunity to invest in a very large production ranch in the heart of cattle country in South Dakota. Offering an exceptional feed base with an above-average water supply, quality fences, and excellent access. The livestock working facilities are strategically positioned for efficiency and the main headquarters and outbuildings are in excellent working condition.

Mungas Ranch

Philipsburg, Montana

A classic Western Montana cattle ranch located in a tightly held region rich in history and agricultural heritage. A year-round cattle ranch with excellent water for irrigation, productive hay meadows and upland grazing pastures for spring, summer and fall grazing opportunities. This is a working cattle ranch with excellent improvements and facilities.

Leffingwell Ranch

Clyde Park , Montana

Fay Ranches represented the Buyer.

Located in one of the premier locations of the greater Bozeman, Montana area, the historic ranch hosts mountain views, creeks, meadow bottoms, and wildlife galore. Surrounded by neighboring ranches protected by conservation easements, the ranch offers solitude without being far from town and little risk of future development. Traditionally operated as a working ranch and dude ranch by the same family since the early 1900s, the history of this ranch runs deep.

Roaring Fork Valley Ranch

Carbondale, Colorado

On a rolling mesa above Colorado’s Roaring Fork Valley, this property borders BLM for direct access to public land. Cattle Creek forms part of the western edge. At roughly 7,300± feet, it offers cooler summers and moderate winters, year-round with 360° views to Mount Sopris and the Elk Mountains. Elk and mule deer frequent the meadows. Eleven 35± acre lots with power, plus water rights to irrigate 200± acres, support recreation, conservation, or phased development, and 45± minutes to Aspen.

Brumley Aspen Waters Ranch

Dunton, Colorado

This Colorado mountain ranch offers aspen groves, spruce, fir, and meadows with live water creeks up from Groundhog Reservoir, offering lush grass for grazing cattle. A thoughtful conservation easement protects the property and provides flexibility, allowing commercial hunting, grazing, timbering, and future homesites. The fishery on the ranch is waiting to be developed further. Elk hunting is stupendous, and world record line class rainbow trout have been caught in Groundhog Reservoir.

Muldoon Creek Legacy Ranch

Carey, Idaho

This Idaho ranch supports 1,300 cow/calf pairs and 400 yearlings. Upgrades to irrigation are planned with NRCS funding. Features include a 3,200 SF home (4BD/4BA, two family rooms) set in a breathtaking river valley against the Sawtooth Mountains. It boasts private access to over 3 miles of fishable waters, rich with brook and rainbow trout, and abundant hunting opportunities for upland game birds and big game. Priority water rights and year-round access are available via Muldoon Creek Road.

Piney Ridge Ranch

Sundance, Wyoming

This premier Wyoming ranch offers a rare combination of privacy, production, and recreation. Set in the western Black Hills, it features a 6,500± sq ft custom log home, a heated indoor arena with stalls and roping setup, and extensive cattle facilities supporting a 225-pair cow/calf operation. Diverse terrain supports trophy elk, deer, antelope, and birds, with two annual landowner elk tags. Ample water includes wells, tanks, springs, and reservoirs. Conveniently located near Upton and Sundance.

Piva Ranch

Challis, Idaho

This Idaho ranch offers exceptional agricultural productivity with extensive water resources, irrigated pastures, and efficient infrastructure for a large cattle operation. Multiple creeks, ponds, pivots, and well-designed facilities support strong hay and livestock production. Scenic river frontage on the Salmon River, abundant wildlife, and mountain views enhance its appeal, while quality improvements and year-round access create a rare blend of performance and functionality.

Black Rock Horse Ranch

Harrison, Idaho

This ranch in Idaho represents a one of a kind ranch ownership opportunity. While currently being operated as a world class equine facility, its location and size make this a trophy acquisition for the discriminating buyer. The views of the lakes, the mild weather and the lush hillsides are remarkable, making this one of the most beautiful ranches in the country.

North Pass Ranch

Bozeman, Montana

Fay Ranches represented the Buyer. An unparalleled Montana oasis within Bozeman, Montana’s newest private, luxury ranch community, Northpass Ranches, is just 15 minutes to downtown Bozeman. This 146± acre property is truly a top-of-the-world experience, with commanding mountain views abound from all angles. This idyllic ranch includes a smartly appointed main house, guest house, and […]

Teton Headwaters Ranch

Driggs, Idaho

This rare Idaho property, held by one family for 30 years, offers fishing on Teton Creek, abundant wildlife, and on-site hunting in complete privacy. Surrounded by conservation easements, it ensures open space, protected habitat, and striking Teton views. Just minutes from Driggs, it balances recreation and agriculture with hay production, grazing, and secure water rights. With growth in Teton Valley and Grand Targhee’s expansion, it offers lasting appeal and strong investment potential.

CloverCrest Ranch on the Jefferson

Twin Bridges, Montana

Situated on the banks of the Jefferson River and multiple spring-fed ponds on site, this ranch property offers a southwestern Montana sporting lifestyle. Fishing enthusiasts will be thrilled to discover 1.5± miles of world-class trophy trout river frontage on the property. The crystal-clear waters of the Jefferson River are home to some of the most impressive trout in the world. The new owner can enjoy exciting hunts for whitetail deer, waterfowl, and upland birds.

Woodchopper Gold Claim

Circle, Alaska

This Alaska gold claim offers an opportunity to own a piece of Alaska gold mining history as with income potential from the gold mining claims. Woodchopper Creek is an inholding in the Yukon-Charley Rivers National Preserve of fee lands and mineral rights only. The ownership includes 15 patented claims and 37 unpatented claims along Woodchopper Creek, a tributary of the upper Yukon River between the towns of Circle and Eagle, Alaska.

Sweet Grass Valley Ranch

Big Timber, Montana

This property offers premier big game hunting for elk, deer, and antelope, along with over three miles of creek frontage and panoramic views of the Absaroka Beartooth Mountains. Featuring irrigated meadows, rolling pastures, and timbered hills, it supports both recreation and livestock operations. Ideally located near Big Timber with easy access to Livingston and Bozeman, it combines natural beauty, privacy, and strong agricultural potential in one remarkable setting.

Nickel Mountain Ranch

Riddle, Oregon

Nickel Mountain Ranch is a unique property for sale, offering diverse investment opportunities and a range of recreational activities. This Oregon ranch combines timbered areas and meadows, providing a picturesque setting to enjoy stunning views and is steeped in Native American history. A rock quarry with easy access offers potential income. The ranch affords exceptional hunting prospects, including trophy-class opportunities for black-tailed deer, Roosevelt elk, black bear, and wild turkey.

Fopiano Ranch

Mitchell, Oregon

A premier cattle ranch with 745± acres of irrigated hay fields and meadows. This ranch offers multiple income opportunities including cattle ranching, hay production and logging. In addition to it’s income opportunities, it’s one of the best big game hunting ranches in Central Oregon and home to a large herd of Rocky Mountain elk.

Rock Creek Cattle Ranch

Philipsburg, Montana

Generational ranches are very special, and this Montana ranch for sale is no different. It offers acreage, river frontage, and has surrounding forests to roam and enjoy the rugged nature of Rock. Rock Creek has flowed through this valley for thousands of years, etching its history into the canyon walls. Fertile soil, lush grass, and approximately 1.5 miles of river frontage offer an abundance of recreational opportunities and untamed beauty.

Aspen Ridge Ranch

Bly, Oregon

Seven lakes and reservoirs backed by senior water rights provide rare control, stability, and year-round operating confidence in south-central Oregon. Designed for productive cattle use, the property includes deeded land, adjoining Forest Service grazing, strong water distribution, wildlife habitat, and recreation. A substantial log lodge, additional cabins, and a manager’s home support owners, guests, or staff, while hydroelectric power with propane backup adds reliable off-grid capability.

MJS Ranch

Located in Madison Valley

Cameron, Montana

Nestled in Montana’s breathtaking Madison Valley near Cameron, this secluded end-of-the-road ranch is bordered by 2.5± miles of National Forest, offering direct access to pristine wilderness. Enjoy sweeping mountain views, abundant wildlife, two year-round creeks, and close proximity to the world-renowned Madison River for fly fishing. Improvements include a custom main home, guest cabin, indoor riding arena, barns, and full ranch infrastructure—ideal for cattle, horses, recreation, and retreat.

Wild Horse Mountain Ranch

Missoula, Montana

A true rarity in the Missoula valley, this large block of land just west of town provides an opportunity for a year-round residence, a recreational retreat or an investment play. The hunting opportunities on site are tremendous and fishing opportunities along the Clark Fork are great.

Northern Plains Grassland and Cattle Ranch

Belle Fourche, South Dakota

This South Dakota ranch’s recent sale includes 11,888± acres of prairie grazing, cross-fenced into several pastures with tanks and dams throughout, the remaining 2,389± acres are dryland hay fields. It features an abundant water supply via a deep well with a pipeline system and concrete tanks, numerous dams, and seasonal creeks. It is located on the plains of South Dakota approximately 20 miles north of Belle Fourche, South Dakota.

Cotton Willow Ranch

Valley Mills, Texas

Pristine live water creeks, natural springs, and rolling native prairie define this exceptional Central Texas ranch. Thoughtful land stewardship has preserved a thriving habitat for abundant wildlife and productive grazing. Improved with multiple ponds, extensive roads, quality fencing, and livestock infrastructure, the property offers outstanding hunting, scenic vistas, premier homesites, and rare accessibility near major Texas metro areas.

Tripple Creek Gold Mine

Nome, Alaska

With patented claims, this active turnkey placer mine produces coarse 91.5% pure gold and valuable sand and gravel by-products that contractors demand. Mining has been nearly continuous since 1997, with current operations underway since 2015. Infrastructure includes highway access, city power, and local equipment rentals. After mining, the land can be subdivided into building lots with proven sales success, offering strong potential for both continued extraction and long-term development.

Stillroven Farm Pheasant & Kennel Club

Berthoud, Colorado

A turnkey sporting property within easy reach of Denver and the Front Range, this offering combines established pheasant hunting and kennel infrastructure with strong flexibility for income and personal use. Managed for upland habitat and privacy, it is well-suited for guided hunts, dog training, boarding, client entertaining, or a membership-based retreat. Productive yet restful, it offers a rare balance of accessibility, open space, and proven operational groundwork.

Old Tobacco Farm

Albuquerque, New Mexico

The Old Tobacco Farm in New Mexico is a green island of alfalfa hay fields in the center of an urban landscape, offering the buyer the opportunity to continue the farming operation, create an urban estate or land bank for the future, or explore the current development environment. The county has approved and adopted a plan for a very valuable 450-residential housing unit development. Outdoor living, art, and history are a way of life in the area. The Sandia Mountains are only minutes away.

East Gallatin River Ranch

Belgrade, Montana

A peaceful 20± minute drive from the booming college town of Bozeman, Montana, the ranch boasts an unheard-of 1.75± miles of both sides of the East Gallatin River as well as a beautiful pond, spring-fed sloughs, and oxbows. A beautiful executive home and guest house overlook the large pond and river with stunning views of the Bridger Mountains and Ross Peak. The setting is private, peaceful, and secluded, yet close to many amenities.

Eagle’s Wing Ranch

Coalmont, Colorado

In Colorado’s North Park, this income-producing ranch offers rare ownership of a contiguous, heavily watered operation with senior water rights and premium bison infrastructure. It includes three well-situated homes, robust hay production, and adjudicated ditches dating to the 1880s. Founded in 1882 and refined by conservation-minded stewardship, the ranch blends agricultural capability, recreation, and lasting value—ideal for buyers seeking meaningful land ownership in the American West.

Fessler Hay & Cattle Ranch

Madras, Oregon

This North Central Oregon ranch offers irrigated farmland, hay ground, and rangeland, ideal for cattle and crop production. With significant water rights, seven residences, barns, workshops, a feedlot, and corrals, it’s a turnkey operation supporting both productivity and comfort. Set against the Cascade Mountains, it combines agricultural performance with recreation and scenic value—an income-producing property with the infrastructure, flexibility, and potential to support long-term success.

Strawberry Ridge Ranch

Colorado City, Colorado

Deriving its name from a wild strawberry patch on the top of a towering bluff, this Colorado ranch for sale offers outstanding big game hunting or watching with an abundant number of species such as trophy elk, mule deer, black bear, and pronghorn antelope. It features a 4,013.45± deeded acres and 640± acre state lease parcel. One of the many features that make this ranch stand out is the valuable water rights, providing 275 acre-feet of water annually for agriculture and municipal use.

Lake Francis Irrigated Farm

Valier, Montana

This highly productive irrigated and dryland farm is set in the shadows of the Rocky Mountain Front and close to the banks of Lake Francis. With meticulous stewardship and well laid out operating systems for efficient farming practices and an excellent history of production, this farm will serve and owner-operator or investment minded buyer long into the future.

Brackett Ranch

Jordan Valley, Oregon

This sprawling Oregon desert ranch for sale is divided by the border between South East Oregon and South West Idaho. This is big cow country made up of rolling sage and grass-covered hills with deep draws. The ranch has the capacity to run 1,000 plus cows year around. The cattle are outside grazing much of the year coming in in the fall to wild meadows and a few months of wild hay feeding.

Maurer Ranch

on the John Day River

Antelope, Oregon

The John Day River winds along this Oregon ranch for approximately 11.5± miles which include 9.5± miles of deeded river frontage, with the balance of the river frontage mostly along BLM lands which are grazed by the ranch! It is one of the few ranches that boasts the rare combination of quality upland game bird, waterfowl, and big game hunting, plus fly fishing for steelhead and smallmouth bass! Rich in history, jaw-dropping vistas, and amazing geology, this ranch has it all.

Flying H Ranch

Downey, Idaho

A rare opportunity to own a fully operational cattle ranch in southeastern Idaho’s productive ranching country. Developed for efficient large-scale livestock production, the property blends irrigated ground with native and improved pastures for disciplined rotational grazing and a direct-to-consumer beef program. Approximately 400± acres under pivot irrigation, durable fencing, and modern infrastructure support high carrying capacity.

Sacred Raven Ranch

Fishtail, Montana

This property lies along Montana’s coveted “Beartooth Front” and is contiguous to thousands of acres of National Forest. The property consists of lush meadows, aspens, conifers, and almost 3 miles of streams and springs, along with a 3,392± SF, 3 bed, 3.5 bath main home, 2,970± SF, 4 bed, 3.5 bath guest home, historic cabin, screened-in kitchen/dining building, and outdoor sauna. Enjoy world-class elk hunting on the ranch and contiguous public land. This property feels private yet is only 1.5± hours to Billings-Logan International Airport, 15± minutes to Fishtail, and 45± minutes to Red Lodge.

Bridger Shadows Farm

Bozeman, Montana

This property is a beautiful 735± acre ranch that has been in the same family operation since the early 1940’s. The Bridger Mountains provide a stunning melodic backdrop with 360-degree views of the entire Gallatin Valley. Located just 5± miles north of Bozeman, this property offers endless possibilities to the new owner.

Los Trigos Ranch

Rowe, New Mexico

This iconic Pecos River property has almost two miles of the trout-filled Pecos River meanders through the middle of the ranch, dotted by majestic cottonwoods and native willows. Deep river pools flow against stunning canyon wall backdrops, providing habitat for 20-inch rainbows, cutbows, and browns. Wildlife including trophy elk, mule deer, black bear, and mountain lion, roam this property. It adjoins the Santa Fe National Forest on the north, offering endless recreational possibilities.

Oxbo Preserve

Bozeman, Montana

This Montana property boasts 1.5+ miles of both sides of the East Gallatin River and mountain views. Wildlife enhancement and stream restoration have made this property a conservation success. With private roads and trails throughout, the property is farmed and maintained, providing hunting for pheasant, deer, & waterfowl. Five minutes from Bozeman & 10 minutes from Bozeman’s airport, this property balances seclusion and accessibility. This is the sale of a third interest in the LLC/community.

Double Angel Lodge

Lewisville, Arkansas

Built in 2006 on the shores of Mays Lake, this lodge features 10 private bedrooms with en suite baths, expansive living areas, chef’s and commercial kitchens, and sweeping views of premier flooded timber. Modern amenities include Starlink Internet, a Klipsch sound system, and multiple gathering spaces. The property offers trophy fishing, exceptional waterfowl, deer, and hog hunting, along with heated shops, equipment storage, and welcoming spaces designed for comfort and camaraderie.

Ninemile Valley Ranch

Huson, Montana

Nestled in the highly sought-after Ninemile Valley, this ranch is 45± minutes from Missoula, Montana. Contiguous to Lolo National Forest for about a mile, this ranch boast views, privacy, and almost two miles of fishable Ninemile Creek. Wildlife includes deer, elk, turkeys, grouse, sandhill cranes, and the occasional wolf. Improvements include a 2,970± SF home, 902± SF log cabin, barn/recreation center that sleeps 22, rustic cabin, two pole-frame storage buildings, and a sporting clays course.

Bangtail Creek Ranch

Livingston, Montana

Most of this acreage is contiguous to National Forest, near Livingston, Bozeman, the Yellowstone River, and Yellowstone National Park. The land boasts views of the Crazy Mountains, Bangtail Ridge, and the Chief Mountain plateau. Wildlife roam through the sage-filled land with newly constructed roads and electricity. This is the ideal location to build your dream home in Montana, as you can enjoy the seclusion of your private property with the convenience of nearby amenities.

Montana Eagle Ranch

Wilsall, Montana

Nestled in the shadow of the Crazy Mountains and contiguous to thousands of acres of National Forest, this property is a little over an hour from Bozeman in the tightly held Shields River Valley. The trout-rich Shields River flows through the property for over half a mile, as well as over a mile of both Mill Creek and Deep Creek, and a little less than half a mile of the South Fork of the Shields River, providing habitat for diverse wildlife. The 1,596± SF, 2 bed, 1 bath log home with loft sleeps 12. Other improvements include a 2 bed guest cabin with outhouse, and a private deck with hot tub and sauna.

Lake Fork Ranch

Leadville, Colorado

This Colorado ranch offers much: 1.5± miles of productive fish habitat-improved Lake Fork Creek, water rights, hunting opportunities, stunning views, easy access to world-class ski areas, the summer jaunt over Independence Pass to Aspen, and recreational opportunities. A golf course, fish hatchery, Turquoise Lake, and the Arkansas River are all neighbors. Whatever draws you to consider this ranch, it is not difficult to see all the possibilities and wonderful attributes that are Lake Fork Ranch.

Shields River Lodge

Clyde Park, Montana

This Montana property, nestled between the Bridger, Absaroka, and Crazy Mountains, has a mile of the Shields River, a guide favorite for fishable trout water, making up the eastern boundary. Run as a fly fishing lodge in the past, the nine-bed, 10.5-bath lodge looks out on incredible views. Located just outside Clyde Park, close to Livingston, and not far from Bozeman’s airport, this property is offered turnkey and is move-in ready for the next owner to begin their Montana adventure.

Golder Ranch on Rosebud Creek

Colstrip, Montana

This legacy property checks all the boxes on your ag, conservation, recreational, and investment property list with a set of working improvements – all within a serene setting rarely available in Montana. The expansive landscape makes it an ideal option for multi-generational families. Its easily-accessible location allows for an authentic Western experience. Grasslands, sub-irrigated meadows, and water rights, make it a highly productive ranch with potential for a conservation easement.

Windcall Ranch

Springhill, Montana

Nestled among the meadows of the Bridger Mountains, with stately Ross Peak serving as the backdrop, lies an exciting opportunity to own land and investment property. The offering hosts five residences, recreational outbuildings, a riding arena, endless trails, and a little piece of Montana. As part of the historic farming community of Springhill, the offering provides a rare opportunity to own a beautiful piece of the Valley of the Flowers near Bozeman, one of Montana’s most charming locations.

White River Ranch

Wamic, Oregon

White River Ranch offers exceptional water resources with 1,427.37 acres of primary water rights ( district and surface rights ) plus 303.2 acres of supplemental water rights. Spanning 2,864.5± acres at the base of Mount Hood, it supports 2,000–2,100 yearlings with six pivots, 16+ lakes and ponds, and flows from the White River, Rock Creek, and Dry Creek. Located in Wamic, this productive ranch includes four homes and organic operations. This is a premier ranching and investment property.

Two Bear Ranch

Big Timber, Montana

This gemstone property combines productive agricultural and irrigated hay land and is located a short distance north of Big Timber, Montana. The ranch is positioned along the banks of Big Timber Creek, and the ranch backdrop showcases the snow-capped peaks of the Crazy Mountains to the west and the Absaroka Mountain Range looming to the south. The views are powerful and welcoming. The Ranch offers 730± diverse acres with excellent upland bird, whitetail, and mule deer hunting.

Bitterroot River Valley Ranch

Hamilton, Montana

On a rare occasion a ranch becomes available with so many amenities that it may excite even those individuals with an exacting list of requirements who yearn for the Montana experience yet provides all the conveniences a nearby town can offer. The Bitterroot River Valley Ranch, an amazing ranch, is an exciting discovery.

Silver Brand Ranch

Bozeman, Montana

Set against Mount Ellis, this end-of-the-road property is less than 8 miles from Bozeman. Privacy, mountain views, wild meadows, pastures, forests, and spring waters surround a 7,632± SF home, a 1,590± SF guest cottage, equestrian facilities, and outbuildings. The 122± deeded acres are bordered on three sides by millions of acres of public land. Whether you’re seeking an equestrian estate, a hunter’s paradise, or a basecamp for year-round adventure, this is a once-in-a-lifetime opportunity.

Four Creeks Sporting Ranch

Big Timber, Montana

This Montana property offers 9± miles of live water and natural pools awaiting a dry fly cast, timbered draws, and shrub-covered hills camouflaging elk and mule deer. The ranch is a blank canvas for new owners to pursue quiet solitude and their favorite recreational activities. Only 29± miles southeast of the small ranching town of Big Timber, Montana, the property presents endless outdoor pursuits and attractive investment opportunities.

The SxS Ranch Estate

Belgrade, Montana

This property encompasses breathtaking views of the Tobacco Root, Bridger, Gallatin, and Madison Mountain ranges in Montana. Much of the property is dedicated to wildlife habitat for pheasants, sharp-tailed grouse, Hungarian partridge, whitetail deer, mule deer, and elk. As part of the exclusive SxS Ranch Reserve, a new owner will have access to 971± shared acres and 1.4± miles of the Dry Creek fishery. The estate features luxurious improvements and additional building opportunities.

Poverty Ridge Ranch

Bone, Idaho

At the base of Caribou Mountain sits Poverty Ridge Ranch, a cattle ranch and premier hunting destination in Idaho. Surrounded by 40,000± acres of public land, it boasts unparalleled access to pristine landscapes. The property features Grays Outlet, a tranquil water source winding through the land, and numerous springs. It offers exceptional wildlife habitat, particularly for elk, deer, and moose, situated in prime hunting areas. A cozy A-frame cabin is ideal for outdoor enthusiasts.

Wapati Point

Big Sky, Montana

A short drive to Big Sky Town Center, 20± minutes to Big Sky Resort, and less than an hour to Yellowstone National Park, this spectacular 9,437± SF home includes 5 beds and 4.5 baths and incredible views of Ramshorn Mountain and the Gallatin Range. A 1-bed, 1-bath guest apartment sits over the detached second heated garage. Sitting on 20± acres in the heart of southwest Montana, this mountain retreat is perfect for the equestrian or someone looking for extra space in an unmatched location.

Slash E Ranch

Island Park, Idaho

Slash E Ranch for sale sits between Island Park, Idaho, and West Yellowstone, Montana, home to the famed west entrance to Yellowstone National Park and is contiguous to Department of Interior land and State Land connecting with National Forest lands leading into Yellowstone Park. Elk, moose, antelope, mule and white-tailed deer, bears, raptors, eagles, wolves, and waterfowl migrate through the property from summer range to winter range and back again, making this a private version of the park.

1805 River Ranch

Three Forks, Montana

Blending Lewis and Clark history with a rare combination of live water and privacy, this turnkey river property lies in the Lower Jefferson River Valley near Three Forks. Featuring Jefferson River frontage, a side channel, a trout-stocked pond, and strong riparian habitat, it supports excellent fishing and abundant wildlife. With quality, move-in-ready improvements and easy access to Bozeman, it offers a secluded yet convenient setting for a private retreat or lasting legacy holding.

Coon Hollow Retreat

Kila, Montana

Positioned in Montana’s Flathead Valley, Coon Hollow Retreat encompasses 3,545± acres with diverse terrain, including timbered slopes, mountain meadows, and picturesque vistas. The property features a vast road network for easy exploration. Conveniently located near amenities yet offering privacy, this serene retreat is an ideal recreational property with endless possibilities and a prime investment for land enthusiasts.

High Alpine Ranch

Big Timber, Montana

This is one of those rare Montana properties that combines fine architecture, wildlife, agriculture, and aquatic features creating a setting like none other. An amazing 3,800± square foot modern masterpiece is surrounded by four spring fed ponds and Big Timber Creek. The property also enjoys stunning views of the snow-capped peaks of the Crazy Mountains to the west and the Absarokee Mountains to the south.

Circle W Ranch

Spray, Oregon

It’s hard to find a ranch that checks all the boxes but this one has all the dimensions of an excellent ranch… river frontage, irrigated farm land, excellent cattle grazing, a BLM lease, timber, fishing and some of the best big game hunting in one of Oregon’s best hunting units. Six L.O.P. tags for Rocky Mountain bull elk and buck mule deer are also available on this ranch. All this and a very nice home!

Browns Meadow Ranch

Kila, Montana

Seldom do we see ranches in a high mountain meadow setting with all of the desirables found at Browns Meadow Ranch. A location in a pristine Montana valley with unmatched privacy and scenic beauty, consistent agricultural production, strong wildlife values, and exceptional recreation. This ranch possesses all of these attributes. These ingredients, along with public land boundaries, lack of conservation easement encumbrances, and a superior location in the Flathead Valley, make it exceptional.

Jefferson River Sporting Ranch

Three Forks, Montana

This Montana riverfront ranch is a premier recreational and agricultural property nestled along the Jefferson River near Three Forks. It features spring-fed wetlands, mature cottonwood groves, and sweeping views of the Bridger, Madison, and Tobacco Root mountains. The land supports abundant wildlife, including deer, moose, waterfowl, and upland birds. With designated homesites and approved septic permits, it’s an ideal setting for a legacy residence or private sporting retreat.

Complete Fly Fisher

Wise River, Montana

Established in 1968, this legendary Montana fly fishing lodge has hosted anglers for nearly six decades on the Big Hole River. Operating as a full-service, turnkey lodge, the property includes guided drift boat fishing, chef-prepared meals, on-site lodging, and an unmatched portfolio of river permits on the Big Hole, Beaverhead, Rock Creek, and upper Bitterroot. With five-star reviews, a loyal global clientele, and six decades of continuous operation, this is a rare and irreplaceable offering.

Springtime Ranch on the Yellowstone River

Big Timber, Montana

Nestled between Big Timber and Columbus along the Yellowstone River, this remarkable Montana ranch offers approximately two miles of blue-ribbon trout fishing frontage. Productive irrigated farmland, diverse terrain of riparian bottomlands, ponderosa pines, and rolling hills create a stunning backdrop. Abundant wildlife roam freely, while two comfortable homes provide the perfect base to enjoy this rare combination of recreational and agricultural opportunity.

Sweetwater Estate

at Agate Creek Preserve

Steamboat Springs, Colorado

Sweetwater Estate at Agate Creek Preserve in Colorado epitomizes luxury and tranquility. This 8,444 sq-ft masterpiece features 6 bedrooms and 8 bathrooms, showcasing meticulous craftsmanship and design. Highlights include a great room with cathedral ceilings and a custom rock fireplace, a gourmet kitchen with high-end appliances, and a private master suite with a spa-like bathroom. Large windows frame panoramic views of the Yampa Valley, offering a serene backdrop for this mountain retreat.

Old Cañones Creek Ranch

Chama, New Mexico

Drive into your own private enchanted forest near Chama, New Mexico. Four trout-filled ponds, two creeks, and exquisite landscaping surround a custom adobe main home and guest home. Stonework, artistic touches, and a stone-and-log gazebo add charm. Three renovated historic log cabins, a guest lodge, barn, and equipment shelter complete the property. Mostly forested with a central meadow, it hosts elk and mule deer. Minutes from Chama and Tierra Amarilla, comes furnished and move-in ready.

Hyalite View Ranch

Bozeman, Montana

Less than 15 minutes from Bozeman, this 137± acre property boasts .7± miles of Hyalite Creek, originating at Hyalite Reservoir and flowing through National Forest before reaching the property. A private drive leads to the 2,888± SF, 3 bed, 4 bath home, as well as a pole barn and horse corrals for the equestrian. Enjoy views of the Gallatin Valley and surrounding mountains from the sunny upper bench, adjoining over 1 mile of Gallatin National Forest, connecting with Yellowstone National Park.

Curly Gulch Ranch

Divide, Montana

Located in the heart of Montana, this exceptional sporting and agricultural property offers premier elk hunting, abundant wildlife, and productive grazing land. Rolling timbered hills and native grasslands provide ideal habitat for elk, mule deer, and antelope, while pristine water sources enhance the landscape’s natural beauty. Featuring stocked trout ponds, spring-fed creeks, and sweeping mountain views, this property perfectly captures the essence of Montana’s ranching and outdoor lifestyle.

Riley Creek Basin

Kila, Montana

A pristine valley ranch outside Kalispell, this property blends rich riparian corridors, mature timber, and productive hay meadows supporting both agriculture and exceptional wildlife diversity. Well-watered with flood irrigation, stock water rights, and natural springs, it offers multiple scenic build sites with sweeping valley and ridgeline views. Free of conservation easements and covenants, this investment-grade Montana ranch is offered for the first time in five generations.

Flying S Ranch

Izee, Oregon

A world class hunting ranch with 284± acres of irrigation, 500± acres of meadows, and heavy stands of timber. This Oregon ranch offers several income opportunities and endless recreational possibilities. With 6 buck deer and Rocky Mountain elk bull L.O.P. tags, no public roads or private holdings within the property lines, this is a one of a kind!

Elkhorn Ranch

Belgrade, Montana

Positioned at the base of the Bridger Mountains, the property sprawls from the forest covered hills and contiguous forest service lands down to lush, productive meadows with mountain streams laden with aspen groves. Numerous building pockets are perfectly positioned to take in the mountains above or the valley below. Wildlife abounds with an elk herd that frequents this ranch along with whitetail, mule deer, pheasant, turkey as well as a variety of other alpine inhabitants.

Dolores River Ranch

Dolores, Colorado

History is woven into this lush 318± acre landscape with a charming 11-bedroom, half-century-old lodge at the base of the now-defunct but delightfully skiable Stoner Ski Area. This Colorado recreational property is located on the Dolores River, dubbed by Trout Unlimited as one of the “Top 100 Trout Rivers in America.” The river is fed by a dozen brook, rainbow, and brown trout streams and is distinguished by riffles, runs, bends, cut banks, and back eddies.

Hidden Springs Ranch

Riverton, Wyoming

This Wyoming cattle ranch offers low overhead, low operating costs, and big production, along with outstanding big game and bird hunting opportunities. It is home to huge mule deer, pronghorn antelope, Rocky Mountain elk, and some of the best chukar hunting available. All the improvements make this a turnkey cattle ranch, including the main home, ranch hand home, bunkhouse, shop, barn, and efficient cattle working facility. Countless “hidden” springs are scattered across the acreage.

Rancho San Ignacio

Sapello, New Mexico

Rancho San Ignacio is a classic Northern New Mexico ranch at the base of the iconic Hermit’s Peak. The adobe hacienda compound frames a spectacular backdrop. The sprawling property combines a rich history, irrigated meadows, well-managed forests, and abundant wildlife. The Sapello River runs for 1.7± miles through the property, providing habitat for hungry brown trout. The murals in the bunkhouse are incredible. Rancho San Ignacio is truly a legacy property!

Crooked Creek Ranch

Winnett, Montana

Lots of water, excellent feed sources, and healthy populations of trophy bull elk make this one of the top hunting ranches in Montana. In the rugged Missouri River Breaks, the ranch is surrounded by thousands of acres of public land. This area is renowned for excellent trophy elk, deer, antelope, and turkey hunting. From high tree-covered ridges to rolling grasslands to timbered coulees and over 300 acres of food plots, this ranch has everything an outdoor enthusiast is looking for.

Over the Cliff Ranch

Forsyth, Montana

Eastern Montana offers a working cattle ranch with a legacy of stewardship and long-term, practical management. Grazing is managed to strengthen grass health, improve water distribution, and build soils, supporting livestock performance while helping the native range recover. Productive pastures and reliable water keep operations consistent. Wildlife and recreation abound with elk, mule deer, whitetail, antelope, and upland birds, drawn by water and native cover across rolling grasslands.

Diamond J Ranch

Ennis, Montana

In 1929, Julia Bennett, a dude ranch pioneer, designed and built this Montana ranch, using architect Fred Wilson, known for The Baxter in Bozeman. Historically a summer guest ranch, this private retreat boasts views of jagged peaks inhabited by elk, moose, bear, and deer. Improvements include a large old lodge, historic cabins, horse corrals, a barn, a pool/pool house, and an indoor tennis court. Water features include Mill Creek and the fishable Jack Creek, as well as a spring-fed trout pond.

Henry Cattle Ranch

Kooskia, Idaho

Henry Cattle Ranch offers a quintessential Western lifestyle amid Idaho’s wilderness, with rolling meadows, pine-covered ridges, and several creek drainages, including Sutler Creek and Red Pine Creek, fostering diverse wildlife. The 2,825± acres near Kooskia include a 4,224± square foot residence, a 3,132± square foot ranch manager’s home, and operational infrastructure like hay fields, timberland, barns, and pastures, with scenic views and recreational opportunities.

Dos Rios Ranch

Pagosa Springs, Colorado

Both the Rio Blanco and San Juan rivers flow through the property, ideally situated in Archuleta County south of the Colorado mountain town, Pagosa Springs. The site supports cattle ranching and hay production, set against the backdrop of the stunning San Juan Mountains.

Big Country Grass Ranch

Judith Gap, Montana

This new to the market opportunity offers an investment-minded buyer looking to explore possible wind energy or solar project near an existing highly productive wind farm located in Montana. This is a unique opportunity to secure a sizeable ranch property that has been closely held by the same family for some time.

Hanging J Ranch

Condon, Montana

Located in Montana’s Swan Valley, this property offers long-held family ownership, exceptional privacy, and expansive mountain views. A custom log home overlooks an 11± acre wetland lake fed by seasonal tributaries, ideal for wildlife observation. The landscape blends timber, meadows, and riparian corridors and directly adjoins US Forest Service land, with public access nearby. Scenic Highway 83 provides convenient access to Condon, Bigfork, Missoula, and western Montana destinations statewide.

Dancing Bear Ranch

Ennis, Montana

This rolling alpine ranch in Montan is a private mountain retreat surrounded by some of the most pristine mountain wilderness in the lower 48 states, yet close to great skiing and fly fishing. Complete with a beautiful traditional Montana home this ranch offers world class recreation right out your backdoor.

The GlobalTerra

Naranjo, Costa Rica

Agroproductive estate in central Costa Rica, positioned between San Ramón, Naranjo, and Zarcero, about 50 minutes from Juan Santamaría International Airport. Built as a coffee estate with strong infrastructure, it now supports two sectors: rotational cattle grazing with organized fencing, roads, and handling facilities, plus a large avocado operation with 28,100± trees. Diverse seasonal crops add cash flow, with recreation and long-term regenerative, ecotourism, and wellness potential as well.

V Timber Creek Ranch

Ennis, Montana

About 10 minutes to Ennis, Montana, only 3± miles to historic Virginia City, and 20± minutes to the Ruby and Madison Rivers, this property borders BLM and State land, providing thousands of acres to recreate on. This ranch boasts staggering views of seven mountain ranges, as well as wildlife ranging from bears and moose to eagles and elk. The property is very diverse, from grassy hillsides filled with flowers, juniper, and aspen trees, to spring-fed valleys teeming with wildlife.

Deep Creek Wildlife Sanctuary

Townsend, Montana

This property boasts 3+ miles of Deep Creek teeming with trout, 400± irrigated acres, and contiguous public land. The Missouri River and Canyon Ferry Reservoir are both just down the road. A mix of forested canyons, native grass, and creek bottom provide terrain suitable for a wide variety of wildlife, including moose, elk, deer, antelope, upland birds, and waterfowl. About an hour from Bozeman and just a few minutes from Townsend, Montana, this property enjoys views of the Big Belt Mountains.

Mountain View Ranch

Powell Butte, Oregon

This Oregon ranch includes an impressive 81,600± square foot equestrian facility, a horse lover’s dream! Complete with 117 horse stalls, two indoor arenas, an office, three large tack rooms, spectator judging areas, a studio apartment, restrooms, built-in waterers, stainless steel stall fronts, concrete alleyways, and two wash rack facilities. In addition, there is an outdoor cutting arena, a heated mare barn with 36 stalls, several farm buildings, irrigated hay lands, and 24 RV hook-ups.

223 E. Main

Bozeman, Montana

This property imbues the Rustic and Elegant elements: complete custom-built interior, wood and tile floors throughout, stone archways and fireplaces, reclaimed wood doors and details, and Pierre Frey wallpaper. 223 E. Main offers a classic example of refined Bozeman living.

Oxbow Crescent

Menan, Idaho

A private peninsula accessible only by land entry or boat, this Snake River property delivers unmatched seclusion along extensive river frontage that connects directly to BLM lands. Irrigated fields, pasture, and waterfowl habitat create a balanced working ranch, supported by senior water rights dating to the 1880s. Whitetail deer, moose, ducks, and geese thrive here, while anglers fish from the riverbank, and a historic homestead with working corrals anchors a proud agricultural legacy.

Burnt Leather Ranch-Steen Place Headquarters

McLeod, Montana

The Burnt Leather is arguably the most coveted recreational ranches in Montana. It provides a window to the very best of the Northern Rockies and a privileged place in nature alongside one of America’s great wildernesses.

Absaroka Moon Retreat

Livingston, Montana

An extraordinary property located in one of the most spectacular settings in North America. Nestled at the foot of the Absaroka Mountain Range near Deep Creek in the northeastern corner of Montana’s famed Paradise Valley, all five structures feature breathtaking views of 9,000 to 11,000-foot peaks – many rising dramatically just 2,000 yards from the main house and others winding 30 miles downrange to the south.

Doc Utterback Ranch

Steamboat Springs, Colorado

Just west of Steamboat Springs, Colorado, the Doc Utterback Ranch spans 1,144± deeded acres. This mountain ranch features varied topography, from open meadows to forests and riparian zones along Tow & Little Tow Creeks. It offers rich big game hunting opportunities, with mule deer, elk, bear, and a recently spotted moose. Awarded for its habitat restoration, the ranch includes 9 springs and is fully fenced with big game-friendly wire, ideal for conservation-focused buyers.

Wyoming’s Star Hill Ranch

Cody, Wyoming

This is truly a unique property that combines the benefits of a serene setting, a myriad of outdoor activities and the comforts of modern living. In today’s fast-paced world, this property provides a safe refuge from the stress and complexity of urban life, providing a place to build unforgettable family memories while reconnecting with nature. We invite you to visit the magic of Star Hill!

Chandler Hereford Ranch

Baker City, Oregon

A rare opportunity to purchase a piece of Western history in Oregon. The Chandler family has raised registered Hereford Cattle at this very location for a continuous period of 131 years. This well-established “Grass Ranch” provides all the necessary ingredients for a discerning purchaser to continue managing the ranch as a year-round cow/calf operation, or to change the operation to a very productive summer cattle grazing enterprise.

Hereford Burnt River Ranch

Hereford, Oregon

A fantastic grazing ranch with irrigated pastures and alfalfa. This Oregon ranch lies in the lush, burnt River Valley with exceptional grass and excellent water rights. The bonus is the prolific wildlife found on the ranch, with elk and mule deer making up much of what folks love about this area. The peace and solitude of this ranch is something special.

Goble Creek Ranch

Rico, Colorado

The Colorado ranch boasts approximately 0.4 miles of both sides of the West Fork of the Dolores River, with exceptional trout fishing for browns and rainbows. Privacy yet convenient access is a hallmark of this property. Paved publicly maintained roads to the ranch driveway allow for year-round use of the property. The log home is amongst an enticing grove of trees near the river. A riding arena, oversized 3-car detached garage, and custom tack room round out the improvements.

Buffalo Jump Equestrian Estate

Three Forks, Montana

The Montana equestrian ranch boasts the most impressive facilities to be admired by elite horse breeders and the most serious horse trainers. A nearly 30,000± square foot heated indoor arena provides horsemen ample space to work year-round in any discipline of the equestrian arts. The ranch dramatically frames the distant Spanish Peaks while quietly perched above the world-famous Madison River below, counting the ranch among premium fishing properties of Southwest Montana.

North Boulder River Ranch

Cardwell, Montana

Nestled in the shadow of Bull Mountain and surrounded by the Elkhorn, Boulder, and Highland Mountains sits this exceptional unspoiled 2,687± acre wildlife-rich ranch. Located just 50 minutes west of Bozeman Montana in the tightly held North Boulder River Valley, land this size in this valley rarely comes to market.

Teton River Farms

Tetonia, Idaho

Located in the Teton Valley, this unique rural community farm offers rich fertile soil for agriculture production, gorgeous views of historical mountains and a multitude of recreational activities making this ideal for a family retreat.

Hope Creek Ranch

Canyon Creek, Montana

This property is in Montana’s pristine wilderness and seamlessly borders 1.5± miles of Helena National Forest, providing access to thousands of acres. Hope Creek meanders approximately 1.12± miles through the property, and three large ponds provide water and allow endless fishing and other recreational opportunities. The property boasts a charming but functional log home, a bunk house, and a barn for equipment and feed storage, serving as the perfect basecamp after a day of adventure.

Mountain Star Ranch

Guffey, Colorado